The Lede

In ten days, both halves of the U.S. bank-core middleware duopoly committed to a frontier-LLM partner.

On May 4, FIS launched its Financial Crimes AI Agent with Anthropic — the bespoke, forward-deployed-engineer deal we covered in Issue #3 ("Anthropic shipped a Palantir"). On May 14, Fiserv answered with agentOS, an entire operating system for agentic AI in banking, built natively across Fiserv's core, payments, issuer-processing, and servicing platforms — with OpenAI and AWS as strategic collaborators. Six financial institutions are co-developing; two — First Interstate Bank and Boulder Dam Credit Union — are running agents in beta today. agentOS reaches general availability in August.

These are not the same product. They are not even the same shape of product. FIS shipped one regulated workflow first — AML — through a professional-services engagement that transfers the build-out as enterprise IP. Fiserv shipped a platform with a marketplace: four first-party agents and nine third-party agents launching alongside agentOS, spanning risk, compliance, deposits, and reconciliation. One is Anthropic playing Palantir. The other is OpenAI playing AWS via Fiserv's distribution layer. Same play; opposite go-to-market motions.

And on May 6, in between the two announcements, Anthropic shipped the bridge between them: ten productized finance agent templates (Pitch builder, KYC screener, earnings reviewer, GL reconciliation, month-end close, financial-statement audit) with native Excel/PowerPoint/Word/Outlook integration and data connectors into FactSet, S&P Capital IQ, MSCI, Moody's, PitchBook, and Morningstar. The FDE motion is no longer the only motion. The bespoke build has a self-serve cousin.

The LLM-vendor battle for finance just stopped being fought at the API price tier. It is now being fought through who controls the bank-tech middleware — and the middleware has named its dance partners.

The Pulse

|

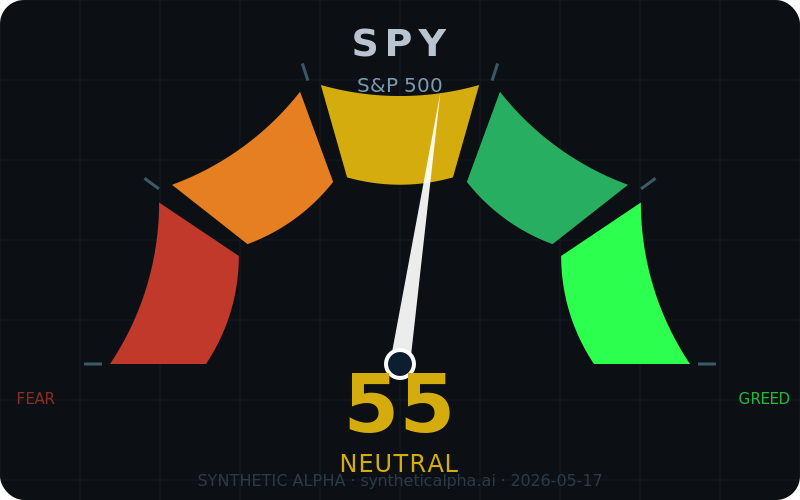

S&P 500 (SPY) — Neutral 55. -1.20% to $739 on 60M-share volume, well below the 75–85M norm — low-conviction profit-taking, not institutional distribution. $730 is the tactical fulcrum; the early-June CPI and mid-June FOMC are the binary that defines H2. |

|

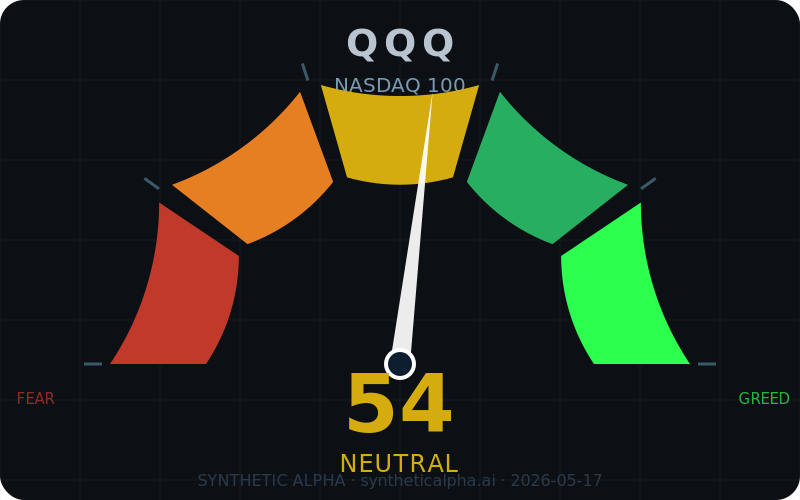

NASDAQ 100 (QQQ) — Neutral 54. -1.51% to $709 lands below the 20-DMA and against the 50-DMA at $695–710. $700 is the make-or-break; a breach of $690 opens $665–675, and July's mega-cap Q2 earnings are the re-rating binary. |

|

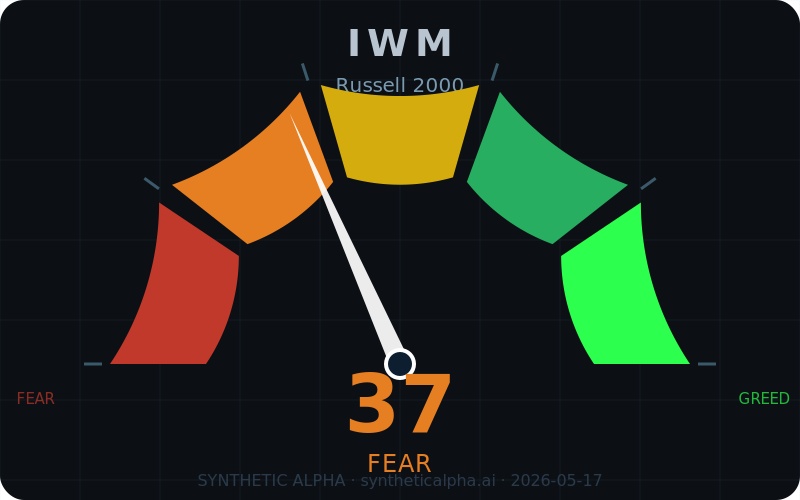

Russell 2000 (IWM) — Fear 37. -2.41% to $277 confirms a full bearish stack — price below the 20/50/200 DMAs and ~75% of constituents on floating-rate debt. The cleanest Fed-pivot trade in the market, with $250 the structural stop. |

|

Crypto (COIN) — Fear 35. -7.82% capitulation to $195 (56% off the $444 high) on elevated volume. Tranche-buyers wait for the $165–175 base or a volume-backed reclaim of $215, with the Senate digital-asset framework vote the next binary. |

Deep Dive - The bank-tech duopoly picked sides

Bank-tech middleware doesn't sell software. It owns the customer.

FIS and Fiserv are the two largest core-banking processors in the United States. Between them, they sit inside the systems of record that move money for roughly 15,000 financial institutions: deposit ledgers, card processing, ACH, payment rails, fraud screening. When a bank decides to deploy AI inside any of those workflows, it is not making a procurement decision against an LLM vendor. It is asking its core processor what's possible. The processor's answer determines which LLM ends up inside the bank.

Both processors just answered.

FIS picked Anthropic. The May 4 launch of the Financial Crimes AI Agent was the visible deliverable, but the contract shape behind it is what makes this a Palantir-class deal: Anthropic's Applied AI team and forward-deployed engineers are embedded with FIS to co-build the product — and, explicitly, to teach FIS how to ship subsequent agents on its own. The named roadmap is credit decisioning, deposit retention, customer onboarding, and fraud. Each one is a multi-quarter forward-deployed engagement. Each one transfers as enterprise IP, not as a SaaS license. BMO and Amalgamated Bank are the first pilots; broader availability is slated for H2.

Fiserv picked OpenAI. The May 14 launch of agentOS is the opposite shape: a platform, not a product, with a marketplace that ships at general availability with four Fiserv-built agents and nine third-party agents covering risk, compliance, deposits, and reconciliation. OpenAI is the frontier reasoning layer; AWS is the deployment surface; six banks are co-developing and First Interstate Bank plus Boulder Dam Credit Union are in beta on commercial-loan onboarding and operational reporting. Where FIS sells the engagement, Fiserv sells the operating system — and the App Store position that comes with it.

The cleanest read of what changed in ten days: the LLM-finance battle is no longer about who has the better model. Both frontier labs are now plumbed directly into the systems of record at every bank that matters. The contested surface is the middleware layer between them. FIS owns one half of the bank-tech market by customer relationship; Fiserv owns the other. Each has now named a sole frontier-LLM partner. The processor's brand sits on the bank's monitor. The LLM's brand sits one layer down.

If you were betting on the LLM picks, you bet on the wrong layer.

Alpha Feed

eToro's CEO and Citadel's CTO take opposite calls on AI alpha — in the same week — CoinDesk · eFinancialCareers

At Consensus Miami, eToro CEO Yoni Assia said AI agents will eventually trade on his platform more than humans will, and disclosed he had spent months training his own quant agent named "Quant" to do exactly that. Citadel's CTO, the same week, said what most of the buy side has been thinking: AI will not produce lasting alpha for hedge funds, because the moment a strategy works it gets copied, and the moment it's copied the edge is gone. Citadel has been running ML in its quant pods for ten years; Ken Griffin himself recently said generative AI has yet to deliver meaningful alpha. The retail-broker view and the multi-strat view are now public, and they don't agree.Crypto wallets are being re-architected for AI agents — Trust Wallet ships an agent kit, implements EIP-8004 for on-chain agent identity — CoinDesk

At Consensus Miami, Trust Wallet announced a developer agent kit and is implementing EIP-8004, the proposed Ethereum standard for on-chain agent identity. Mesh executives on the same panel argued wallets — not L1s — become the trust boundary once agents start moving money on a user's behalf: the wallet vouches that the agent is authorized, holds the keys, and signs the transaction. This is the DeFi-side mirror of Issue #3's Visa-and-Mastercard agent-credentials story. Same problem; opposite stack. The fight to be the trust layer between an autonomous agent and money that moves is on.AI agents already run ~20% of DeFi — and still lose to humans at trading — Decrypt

Agent-managed positions on-chain have crossed $39 million in TVL and represent roughly a fifth of DeFi agentic activity. The inconvenient data point: net P&L for agent-managed positions still trails human-managed positions on the same protocols. This is the rare quantified pushback in a space dominated by vibes — and a useful counter-anchor for the eToro-vs-Citadel question. The agent buildout is happening. The agent-as-alpha case is not yet supported by the data.

The Position

AI is a double-edged sword in finance. That's not a hot take — it's just true.

The middleware just told you where the money lands.

The bull case is real. Agents are arriving whether or not they produce alpha. FIS, Fiserv, Goldman Sachs (Claude running trade accounting and client onboarding), and Bank of America (Salesforce Agentforce rolled out to 1,000 financial advisors) are all moving from pilot to production this year. Regulators are making space. Anthropic's ten finance templates and Fiserv's nine-agent marketplace are both shipping at scale-able prices, not bespoke quotes. The productivity story has receipts.

The bear case is also real. Citadel's argument — that AI alpha gets arbitraged the moment it works — is the inconvenient one. And the only quantified DeFi data point this week shows agents still losing to humans on net P&L. If alpha is the bet, the case is open at best.

Our take: alpha may be a wash. Middle-office is where margin actually compresses — KYC, onboarding, reconciliation, month-end close, AML investigations — and that is exactly the workflow set Anthropic just productized and Fiserv just put a marketplace on. The interesting bet is not which LLM wins. It is which middleware vendor captures the most workflow per institution before the third one shows up.

Bet AI-as-alpha — or bet the middleware?

We're watching the second one.

Stay safe, build safe, trade safe.

On The Radar - The third bank-tech middleware

Two announcements is a coincidence. Three is an industry pattern. FIS chose Anthropic; Fiserv chose OpenAI; the open seat is whichever core-banking middleware vendor announces an LLM partner next.

The candidate list is short: Jack Henry (serves the U.S. community-bank tier), nCino (commercial lending), Temenos (international core), and credit-union-focused Corelation.

What to watch in H2 2026: any of those four naming a frontier-LLM partner with named co-development banks. The first to do so confirms the duopoly pattern is becoming the industry shape — and tells you whether Google's Gemini and Meta's Llama get a seat at the table at all. The clock starts now.

Synthetic Alpha publishes every Monday at 6am Eastern.

Forward this to someone who needs to know what's actually happening in AI and finance.